Household Digital Consumer Behaviour 2023

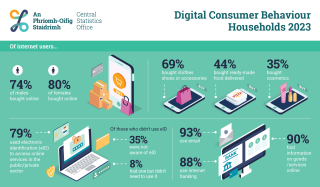

A recent report from the CSO, 'Household Digital Consumer Behaviour 2023' found that using email is still the most popular internet activity with 93 per cent of internet users surveyed in 2023 saying they used email, up from 91 per cent in 2022. The second most popular internet activity was looking for information on goods or services with 90 per cent of users engaging, followed closely by 88 per cent using the internet or mobile phones for banking or payments.

Online Shopping

A section of the report examines how the internet is used to make purchases. They found that the internet is "being used for everything from financial transactions to online shopping (food, clothes, etc.) and cultural and sporting events. There are some differences between men and women in what they use the internet for, with different experiences by type of household also".

Overall, online shopping decreased slightly, from 81 per cent of internet users in 2022 to 78 per cent in 2023. However, households with children bought more online, 94 per cent of two adult and 91 per cent of one adult compared with 88 per cent of households with no children. Only 8 per cent of those using the internet have never bought or ordered either goods or services online.

Clothes, shoes, or accessories (including bags, jewellery, etc.) continues to be the most common purchase online according to 69 per cent of internet users. This is a decrease from 71 per cent in 2022. Sports gear purchases (includes sports gear and equipment but excludes sports clothing) online are slightly up from 20 per cent in 2022 to 21 per cent in 2023. The report notes a gender difference with 74 per cent of females buying clothes, shoes or accessories online compared with just 60 per cent of males. 22 per cent of internet users bought "computer tablets, mobile phones or accessories online in 2023 compared with 27 per cent in 2022, while one in six (16 per cent) purchased consumer electronics (TV sets, stereos, cameras, etc.) or household appliances (washing machines, etc). Also, the online purchase of medicine or dietary supplements increased by six percentage points in 2023 – 20 per cent of internet users compared with 14 cent in 2022.

Financial Literacy Online - Buy Now, Pay Later

A recent Consumer Research Bulletin from the Central Bank of Ireland, 'Buy Now Pay Later Consumer Insights Update', showed that many customers using a Buy Now, Pay Later option do not realise that this is a form of credit. Simply, buying with Buy Now, Pay Later means that a first payment is paid when the goods or services are bought. The next payments are paid off at an agreed rate and intervals. This delayed payment option is actually a loan and is owed to the Buy Now, Pay Later lender. Usually, no interest is charged on that loan portion but many agreements can have administration, late or missed payment fees attached.

Key Findings

- While the availability of Buy Now, Pay Later is becoming more common, there is limited experience amongst Irish consumers of Buy Now, Pay Later at present. Only 15 per cent of Irish adults report that they currently use Buy Now, Pay Later or have ever used it previously. However, Buy Now, Pay Later is increasingly being considered by Irish consumers with 24 per cent reporting they would consider it to fund a purchase in the future.

- Buy Now, Pay Later users tend to be younger in age (25-44 years). Those who currently or have previously used Buy Now, Pay Later are also more likely to be accessing other forms of credit, reporting higher rates of borrowing compared to the rest of the population.

- Buy Now, Pay Later appears to be associated with instances of impulsive shopping or unplanned, excessive spending. 38 per cent of Buy Now, Pay Later users agree that Buy Now, Pay Later has made them ‘more likely to purchase things they don’t need’ and 43 per cent agree they ‘often spend significantly more money than planned when they use Buy Now, Pay Later’.

- The findings indicate a lack of understanding on the part of consumers availing of Buy Now, Pay Later credit. Consumer knowledge of Buy Now, Pay Later tends to be limited, with 22 cent of users reporting not having a full understanding of the credit product.

- There are fundamental consumer misconceptions regarding what Buy Now, Pay Later actually is. The research identified that many Buy Now, Pay Later users (36 per cent) seeing it as a payment method rather than a form of credit. We found that when availing of Buy Now, Pay Later, consumers tend to be focused more on the monthly payment amount rather than the total amount borrowed at the point of purchase.

Financial Inclusion

Financial services are becoming increasingly digital, with more and more daily, everyday transactions moving on-line or becoming cashless. The restrictions experienced during Covid-19 related lockdowns, proved difficult for those that did not have the ability to make payments for goods with cards, either in store or on-line. Access to financial services, now more than ever is key to inclusion in society. With the publication of the White Paper to End Direct Provision and to Establish a New International Protection Support Service committing to facilitating the opening of bank accounts for International Protection applicants - the Basic Payment Account - the spotlight is once again on the importance of financial inclusion.

Financial exclusion is not just about access to bank accounts but access to reasonable, affordable credit that takes account of the financial position of the consumer while cognisant of the need for people on low incomes to meet contingency expenditures without resorting to high cost credit, ‘pay day loans’ and ‘home credit companies’ which can charge APRs of up to 287 per cent. Illegal moneylenders are also in operation. Credit unions have traditionally provided low cost credit to members within their ‘common bond’ area charged at 1 per cent interest per month, or 12 per cent per annum. These loans are provided as an alternative to high cost credit from legal and illegal moneylenders for families having difficulties saving for life events such as a child’s communion, home improvements or the unexpected breakdown of an essential appliance.

A 2022 study by the Economic and Social Research Institute found that 6 in 10 people face unexpected expenses each year. Considering then that in 2018, almost four in ten people (37.3 per cent of the population) reported being unable to meet an unexpected financial expense, access to affordable short term credit or the ability to accrue savings in vital.

The Inaugural Central Bank of Ireland Financial Services Conference took place in November 2022 with the theme ‘Supporting the Economy, Delivering for the Consumer’ and noting “the importance of education for consumers...to help them make better …. decisions. Financial literacy is becoming increasingly important in the context of technological innovation”. Who provides that education is key so that it is not simply companies selling products under the guise of education or literacy or training.

The National Adult Literacy Agency (NALA) Report ‘Financial literacy in Ireland’ recommends ‘more education and training on financial literacy. This involves the development of literacy, numeracy and basic computer skills, which underpin everyday financial activities”. This will increase the skill levels of individuals to understand the financial products and services they engage with. However, the companies selling financial products and services also need to ensure that consumers fully understand the information they provide. An approach, similar to plain English is taken in the U.K. by Plain Numbers as they work with firms, changing the way information is conveyed to ensure increased comprehension of bills and financial contracts.

In light of the severity of its impact, Social Justice Ireland welcomed the inclusion of financial literacy in the Roadmap for Social Inclusion 2020-2025 and urges Government to build a module on financial literacy in to the primary and secondary curricula. It is incumbent on Government to track levels of financial exclusion and to build and monitor policies and practices aimed at eliminating it in its entirety by 2025. Also welcome is the commitment in the Report on the Retail Banking Review, published in November 2022, that Ireland should fulfil certain OECD obligations in the area of financial literacy and develop a national financial literacy strategy. The Department of Finance has been tasked with the development of this national financial literacy strategy and work is currently underway.